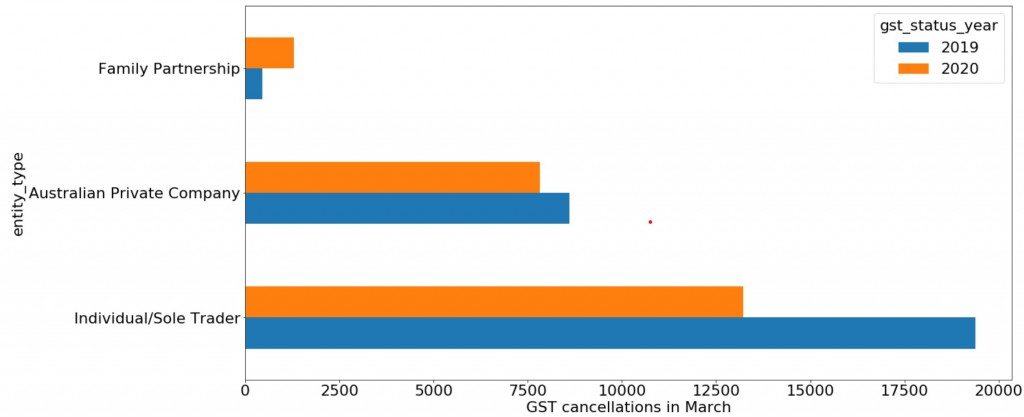

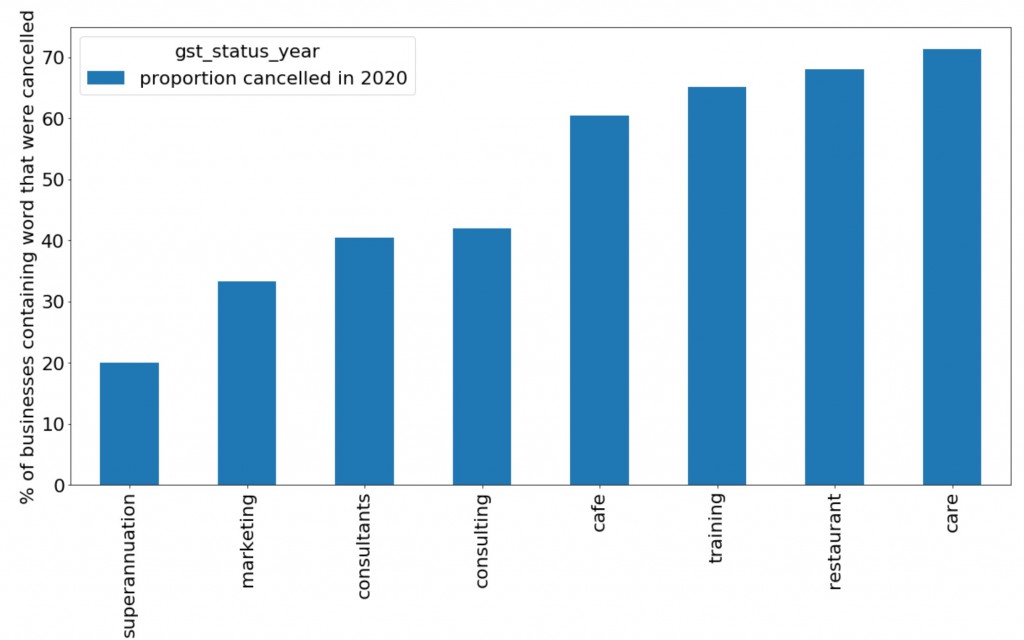

A Microburbs analysis: I analysed every polling booth’s vote in yesterday’s federal election to find high resolution insights on where Australian politics is heading.

Most of the commentary we see so far is on an electorate level, but there are far more polling booths than electorates, so we can much more confident about analysis at this level.

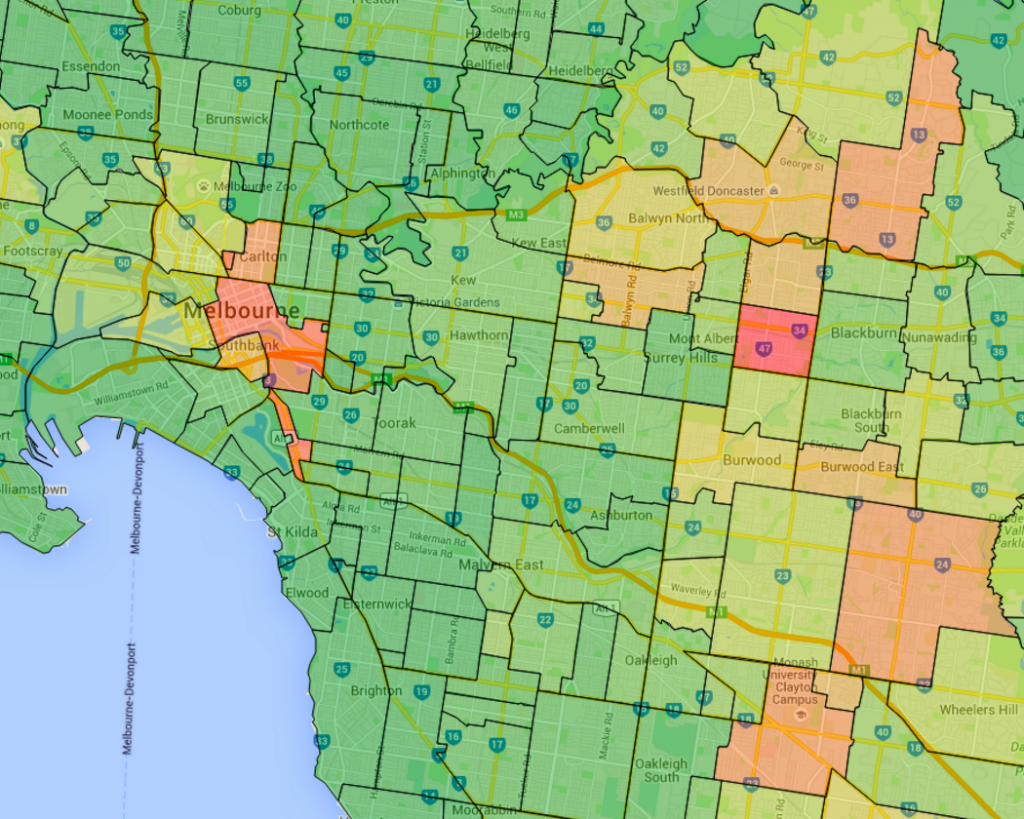

Coalition continues to trend poor

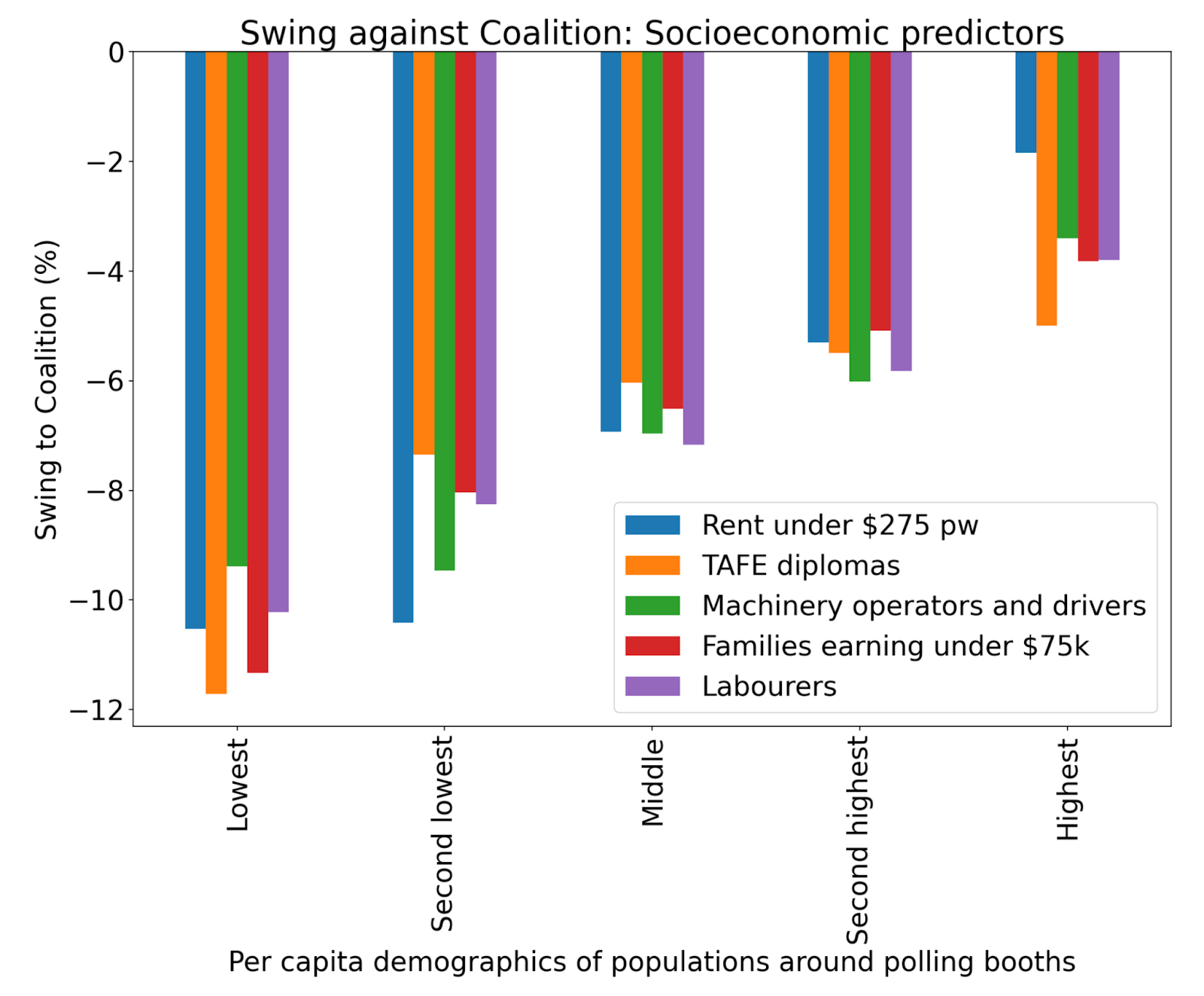

The big takeout is we’re seeing a continuation of the trend in the federal last election where the Coalition’s support base is shifting towards poorer, less skilled, the less educated people born in Australia.

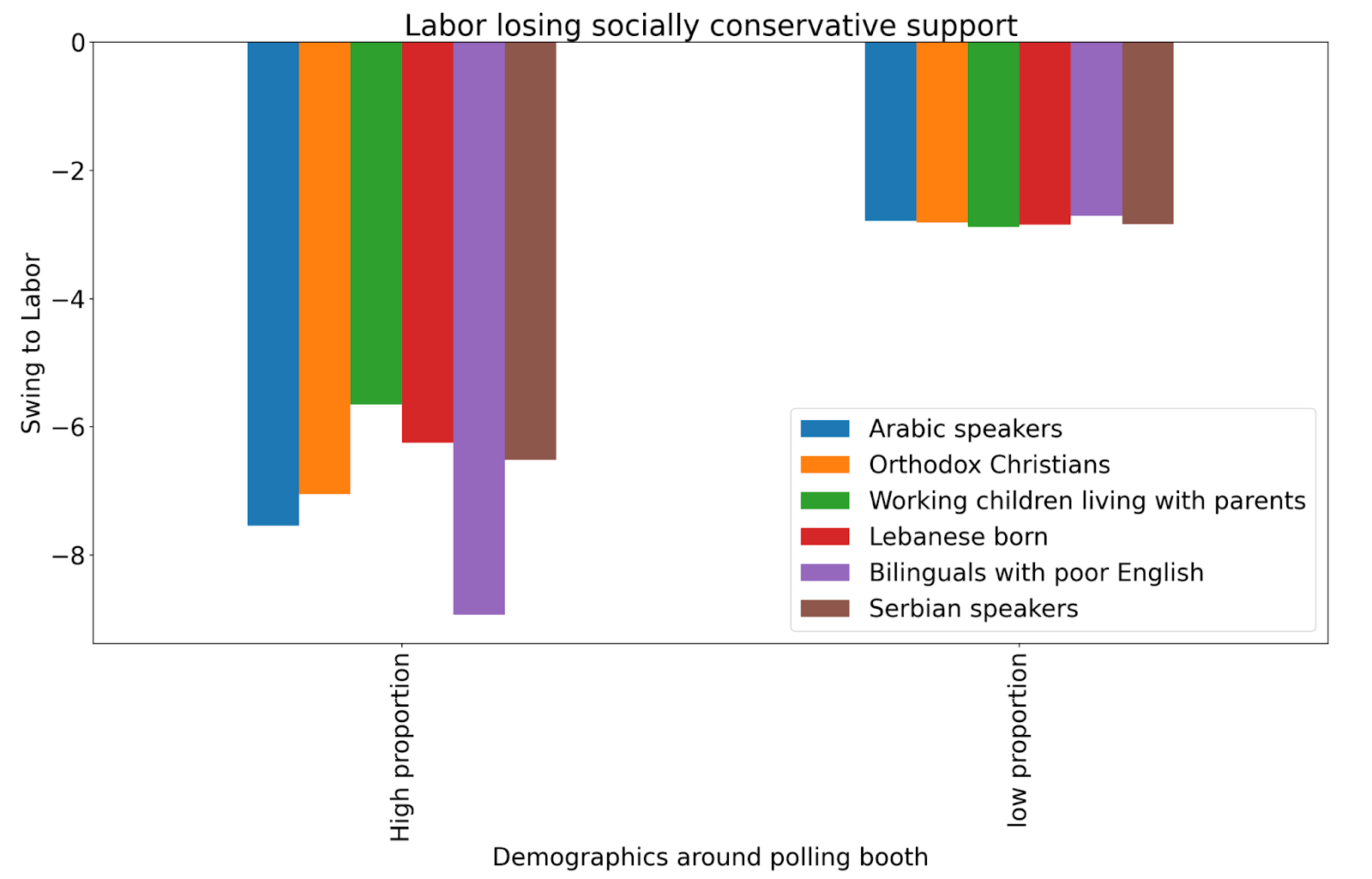

Increasingly the Coalition represent the Australian-born working class, as independents deprive them of their previous base of rich, professionals. Labor is losing social conservatives seemingly to the minor right wing parties.

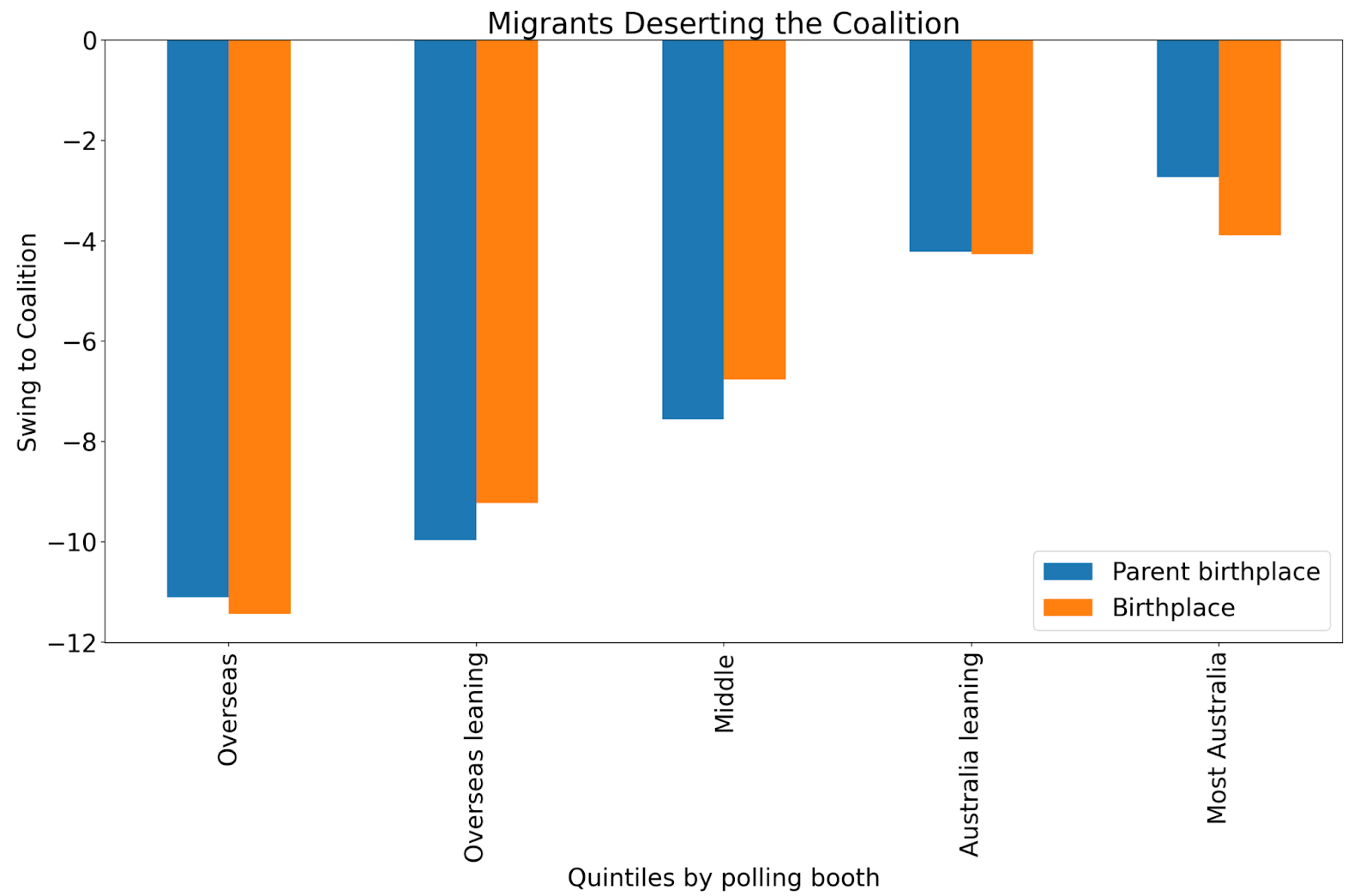

The top 20% of polling booths with the most international citizens, swung against the Coalition nearly 12%, while the most polling booths with a majority third generation ancestry only suffered a similar swing against them to what Labor endured nationally.

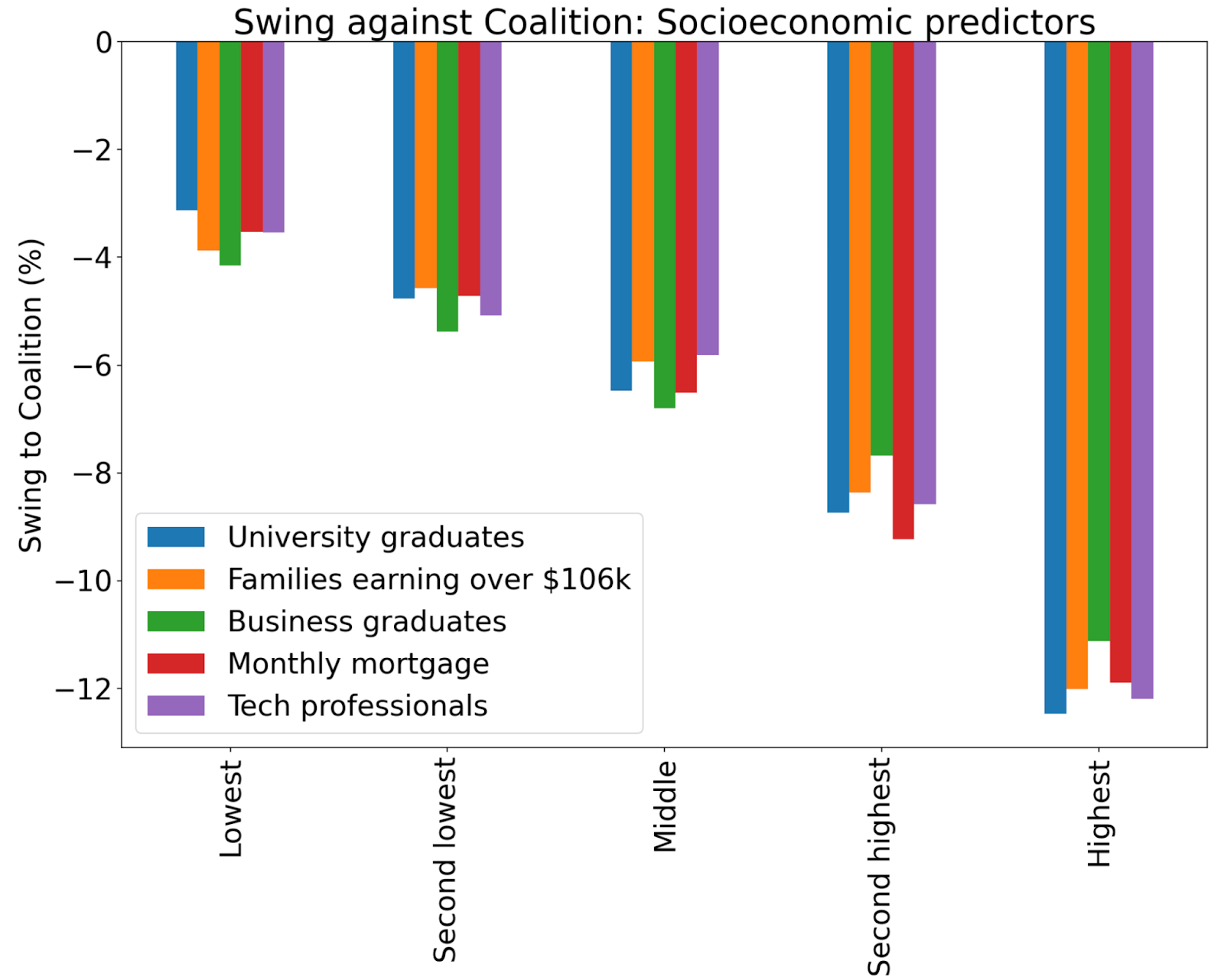

Rich, educated professionals swung 11-12% against The Coalition, while the country’s working poor swung only 3-4% against them.

So 20% of polling booths with paying the lowest rent, earning the lowest incomes and with the least skills swung 2-4% against the government, while the fifth of Australia’s polling booths where such people are rarest saw a 10-12% collapse in LNP primary vote.

Labor wins back miners

The best predictor of a swing to Labor were miners. The 665 polling booths in the country who had over 5% of the population in mining, Labor enjoyed an average swing to them of 1.5% while the rest of the country swung against them 3.5%.

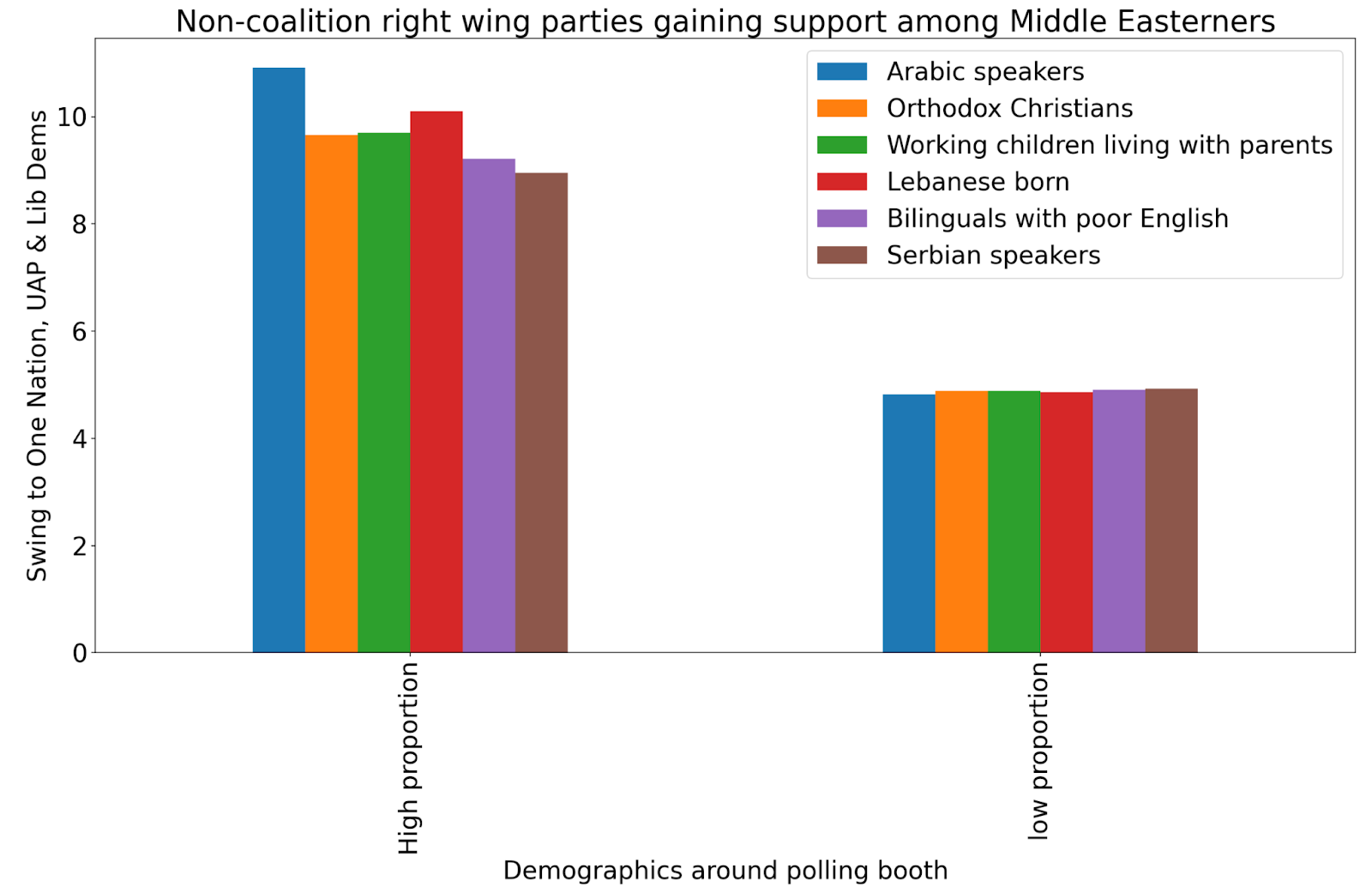

Minor right wing parties grow among Middle Easterners

Perhaps due to anti-vaccination, anti-lockdown sentiments and common social conservatism, the minor right wing parties have surged amongst people of Arabic and Serbian background. Where the polling booth is in the top 5% of these demographics, such parties more than doubled their swing.

There is a matching swing against Labor in these same places.

There will be plenty more demographic analysis to come with the coming reboot of Microburbs for 2022.

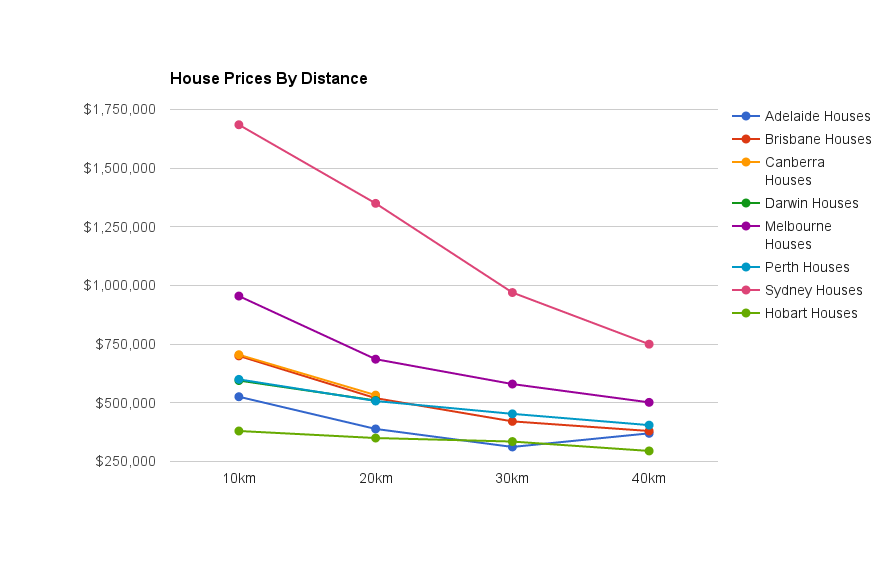

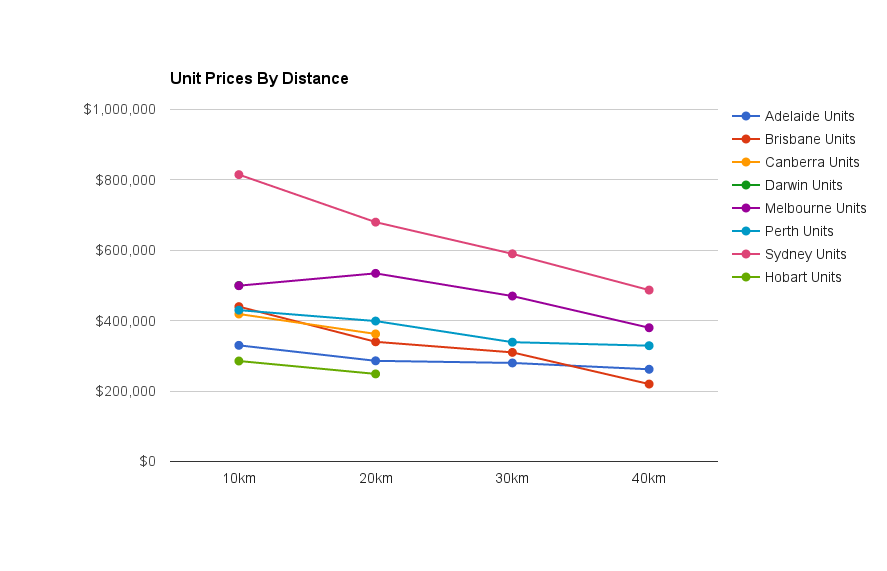

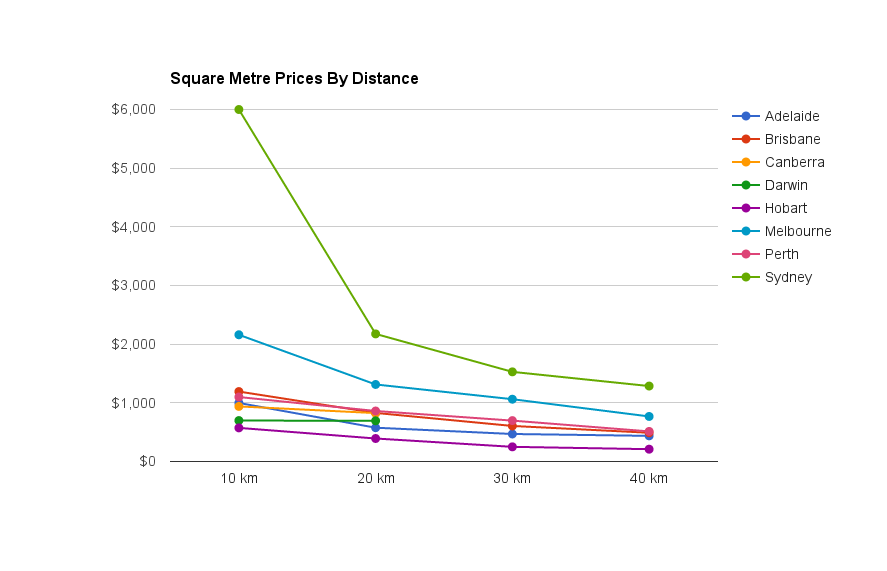

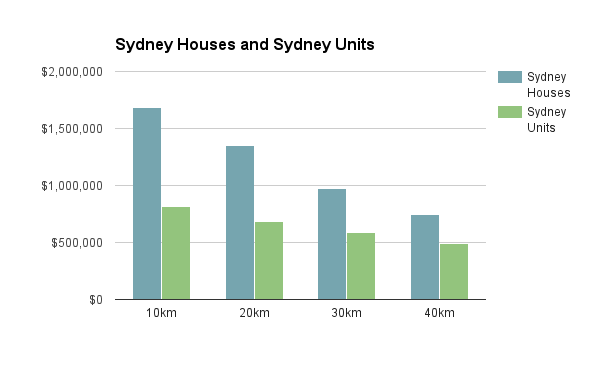

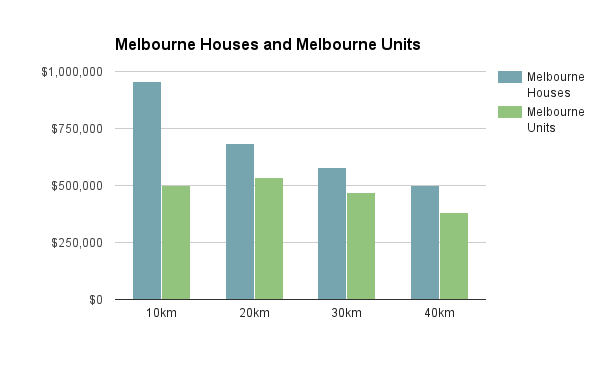

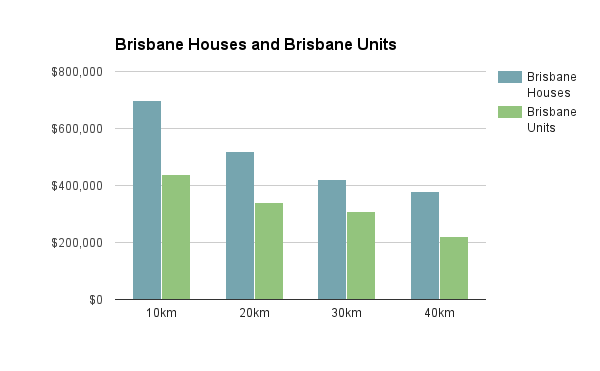

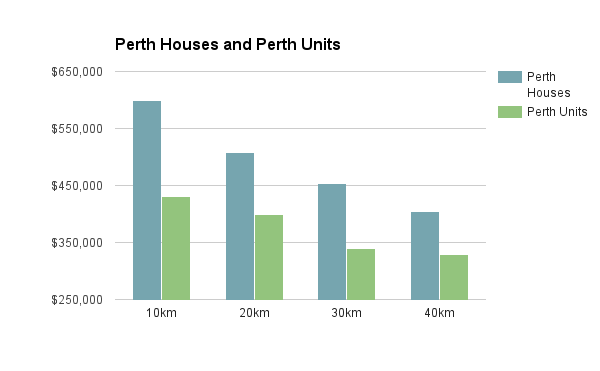

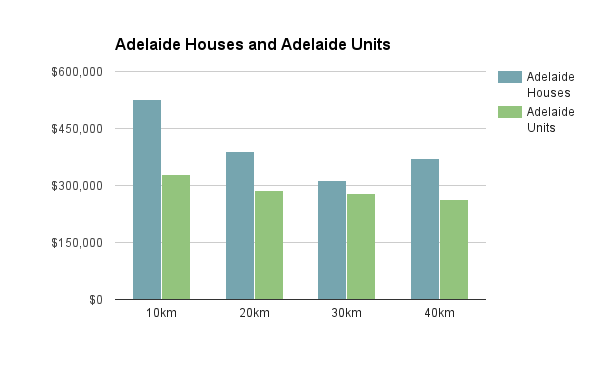

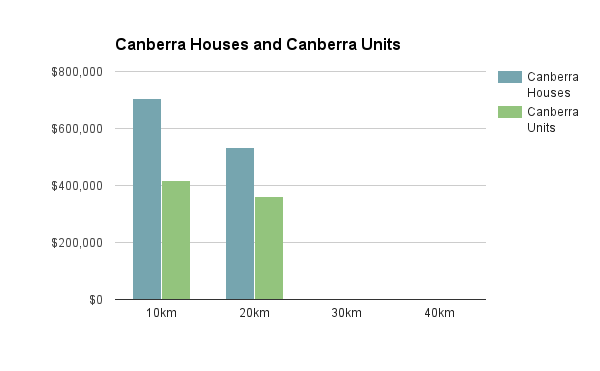

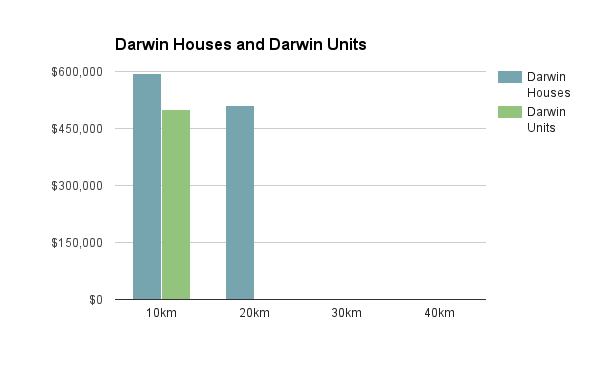

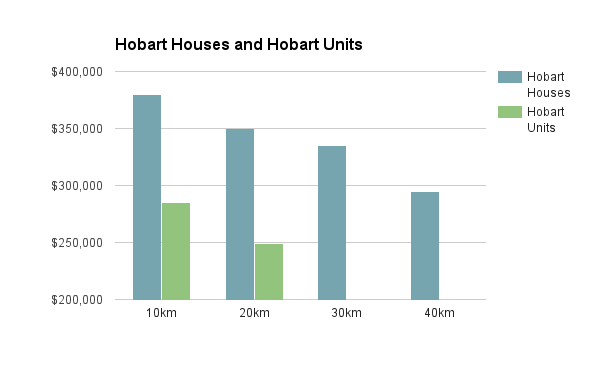

First we’ll look at house prices for all state capitals, grouped by whether they are 0-10km from the centre of the city, 10km-20km and so on. For instance, we can see that if we had a $600,000 budget, we could look at central Perth or Adelaide, 10-20km from the centre of Brisbane or Canberra, 20-30km from the heart of Melbourne and more than 40km from the middle of Sydney.

First we’ll look at house prices for all state capitals, grouped by whether they are 0-10km from the centre of the city, 10km-20km and so on. For instance, we can see that if we had a $600,000 budget, we could look at central Perth or Adelaide, 10-20km from the centre of Brisbane or Canberra, 20-30km from the heart of Melbourne and more than 40km from the middle of Sydney.

Unlike the Erskineville, Newtown, Camperdown troika, Forest Lodge stands alone at serving both families and hip people with neighbouring Glebe to its east serving hipsters and more spacious Annandale to its west providing for family.

Unlike the Erskineville, Newtown, Camperdown troika, Forest Lodge stands alone at serving both families and hip people with neighbouring Glebe to its east serving hipsters and more spacious Annandale to its west providing for family.

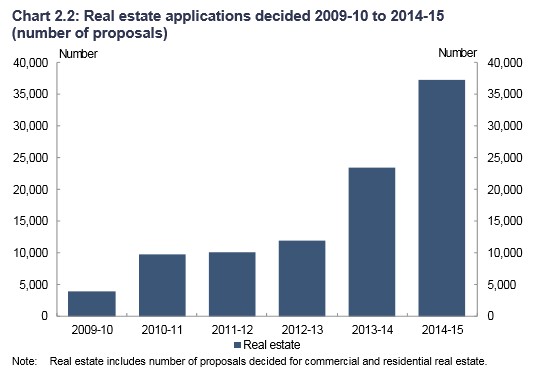

Image source: FIRB

Image source: FIRB