This week has seen the Reserve Bank of Australia cut the cash rate to a historic low of 1.5%. The announcement was not a surprise to many, with low inflation data signalling a likely cut in the lead up to the RBA board meeting.

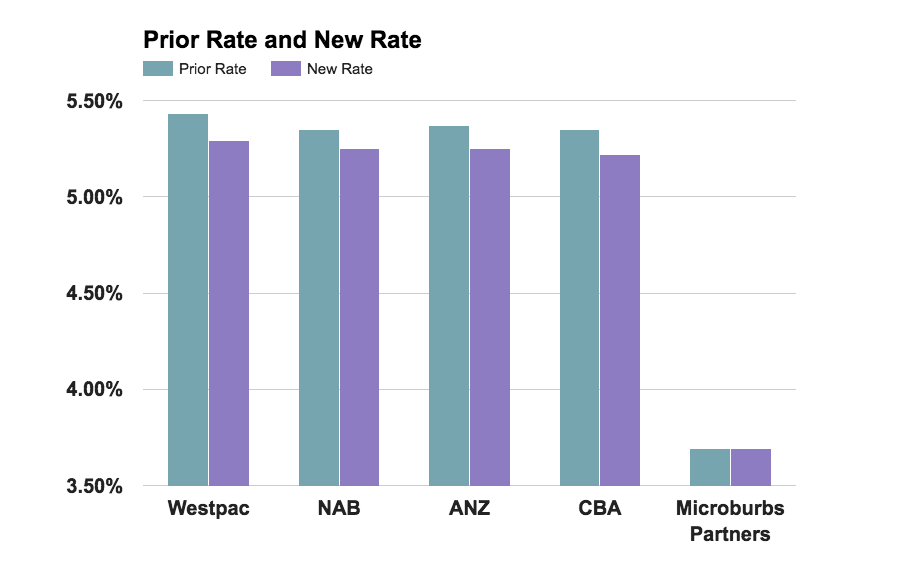

What has been a surprise is the response from the big four banks. Rather than pass on the full rate cut to their mortgage customers, they reduced their standard variable rates by only half as much as the rate cut, and increased term deposit rates, rather than cutting them. More surprising still, was the swiftness and similarity of announcements by CBA and NAB, with Westpac and ANZ trailing after.

Many have been left feeling frustrated and powerless after being stuck around the 5.3% mark while the cash rate approaches zero. There are alternatives though, which dozens of lenders available outside the big 4 with much fairer rates. Mortgage holders can compare personalised offers from a wide range of lenders in 2 minutes without filling in application forms and navigating red tape. You can even give it a go right now.

It’s easy to brush off the idea of changing lenders for a rate cut as being not worth the hassle, but that couldn’t be further from the truth. A reduction in interest rate brings the power of compound interest over to your side. Every 1% per year on every $100K of your loan is $1000 a year into the household budget. Furthermore though, you save on the compound interest on that. A better rate can mean reaching financial freedom years earlier, building an investment portfolio while paying down your mortgage or having the money to travel again.

Get some offers in 2 minutes and look at how much you could save over the life of your loan.